TEL:4006258268

FAX:020-36657099

E-mail:service@gzhw.com

Info E-mail: grand.tt@grahw.com

Address: 18th Floor, Global Trade Center, No. 148 Xingang East Road, Haizhu District, Guangzhou, China

Industry Information

Location:Home > News > Industry Information > DetailIn-Depth Industry Analysis: An Overview of China's Fur Industry Chain, Market Size and Competitive Landscape in 2021

China's Fur Industry Maintains a Steady Economic Development Momentum

Fur refers to garments made from animal fur, featuring an elegant appearance and a relatively high price. In recent years, China's fur industry has maintained a steady development momentum in its economic operation, with annual sales remaining between 40 and 50 billion yuan. Since the outbreak of the COVID-19 pandemic, the domestic and international business environment has become increasingly challenging, bringing mounting downward pressure on the fur industry. Meanwhile, under the backdrop of regular pandemic prevention and control, there are opportunities amid the hardships for the industry.

Also known as fur pelts or dressed fur, fur is a mid-to-high-end commodity widely used in various fashion garments. Its combination with down, textile fabrics and other materials has expanded its application scope, consumption seasons and consumer markets.

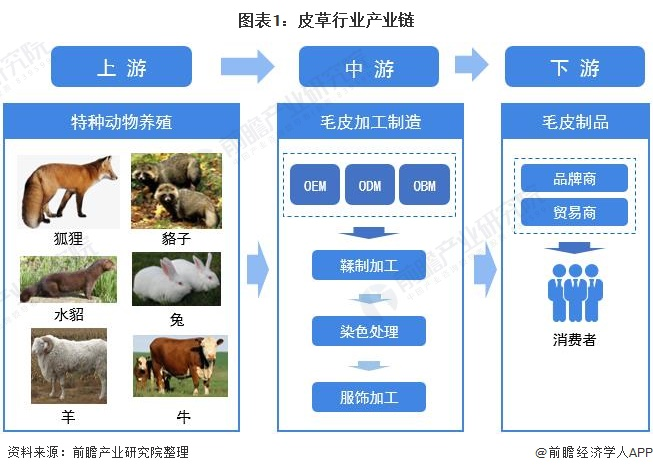

1. Industrial Chain of the Fur Industry

The fur industry chain mainly includes the breeding of fur-bearing (special) animals, fur tanning, dyeing, processing, as well as the design, manufacturing and marketing of fur garments.

· Upstream: The fur animal breeding industry, a high-value-added special breeding sector, focuses on the artificial rearing and breeding of domesticated animals such as minks, foxes, raccoon dogs and rex rabbits to obtain fur and other animal products.

· Midstream: The fur processing industry, which takes fur as raw material and produces fur garments and products through mechanical processing, manual sewing and other processes.

· Downstream: The sales of fur products (domestic and export) and end consumers.

Chart 1: Industrial Chain of the Fur Industry

2. Analysis of the Upstream of China's Fur Industry Chain: Continuous Decline in the Skin Output of Major Animals

The upstream raw materials of the fur industry are mainly the fur of minks, foxes, raccoon dogs and other animals. In recent years, the market for mink, fox and raccoon dog skins in China has generally been in a state of oversupply. The total skin output of minks, foxes and raccoon dogs in China showed a downward trend from 2013 to 2019.

In 2019, the output of mink, fox and raccoon dog skins in China reached 11.69 million, 14.43 million and 13.59 million pieces respectively. The output of mink and fox skins decreased by 43.61% and 17.02% year-on-year, while that of raccoon dog skins increased by 10.22% year-on-year.

On May 29, 2020, the Ministry of Agriculture and Rural Affairs officially released the Catalogue of National Livestock and Poultry Genetic Resources approved by the State Council, which included four fur-bearing animals: "mink (non-edible), silver fox (non-edible), arctic fox (non-edible) and raccoon dog (non-edible)".

This means that the artificial breeding of minks, silver foxes, arctic foxes and raccoon dogs is no longer classified as the "breeding and reproduction of wild animals", but incorporated into animal husbandry. This is a major and prudent adjustment to the fur animal breeding industry, of great significance for the sustainable development, transformation and upgrading of the entire industry.

Chart 2: Skin Output of Minks, Foxes and Raccoon Dogs in China, 2013-2019 (Unit: 10,000 pieces)

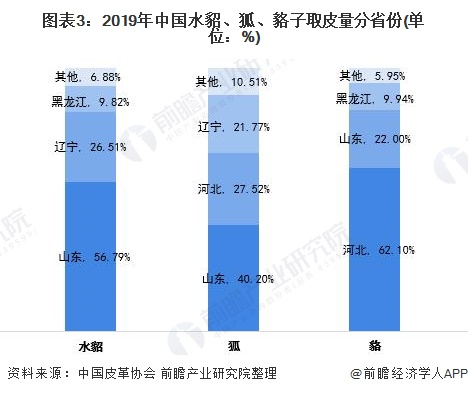

In terms of the regional distribution of the skin output of major animals, the raw materials of China's fur industry are mainly concentrated in Shandong, Hebei, Liaoning, Heilongjiang and other provinces. Specifically, Shandong Province had the largest mink skin output, accounting for 56.79% of the national total in 2019; it also ranked first in fox skin output with a share of 40.20%. Hebei Province was the top producer of raccoon dog skins, accounting for 62.10% of the national output in 2019.

Chart 3: Provincial Distribution of Mink, Fox and Raccoon Dog Skin Output in China, 2019 (Unit: %)

3. Decline in the Industry's PPI Under the Impact of the Pandemic

According to the statistics of the National Bureau of Statistics, affected by the pandemic, the monthly Producer Price Index (PPI) of China's fur tanning and manufacturing industry has been declining since 2020. Specifically, the PPI stood at 100.5 in January 2020 and dropped to 95.6 in December 2020. In January 2021, the PPI of the fur tanning and manufacturing industry rebounded slightly.

Chart 4: Monthly PPI of China's Fur Tanning and Manufacturing Industry, 2019-2021 (Same period of the previous year = 100)

4. Analysis of the Midstream of China's Fur Industry Chain: Opportunities and Challenges Coexist Amid the Pandemic

(1) Growth in the Number of Above-Scale Enterprises in China's Fur Industry

After years of development, China's fur industry has entered a period of steady development. From January to August 2020, there were 7,846 above-scale enterprises in China's core leather industry (footwear manufacturing, bag and luggage making, leather tanning, leather garment production, fur and fur products), among which 543 were fur and fur products enterprises, a net increase of 22 compared with 521 at the end of 2019.

Chart 5: Number of Enterprises in China's Leather Industry and Fur & Fur Products Industry, 2019 and Jan-Aug 2020 (Unit: piece)

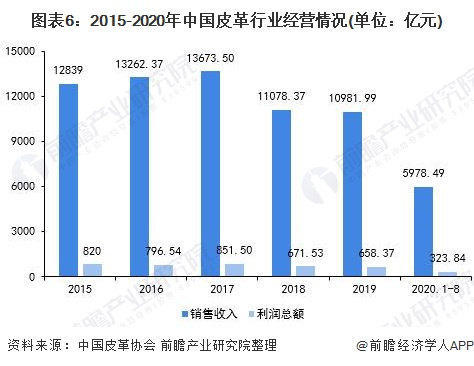

(2) Sustained Decline in the Market Size of China's Fur Industry

In recent years, the development environment of the national fur industry, both at home and abroad, has been tough. From 2015 to 2019, the overall market size of China's above-scale core leather industry showed a downward trend. In 2019, the industry achieved sales revenue of 1,098.199 billion yuan and total profit of 65.837 billion yuan, a year-on-year decrease of 0.87% and 1.96% respectively.

From January to August 2020, affected by the COVID-19 pandemic, the leather industry continued to decline, with a cumulative sales revenue of 597.849 billion yuan and total profit of 32.384 billion yuan, a year-on-year drop of 16.34% and 24.86% respectively.

Chart 6: Operation of China's Leather Industry, 2015-2020 (Unit: 100 million yuan)

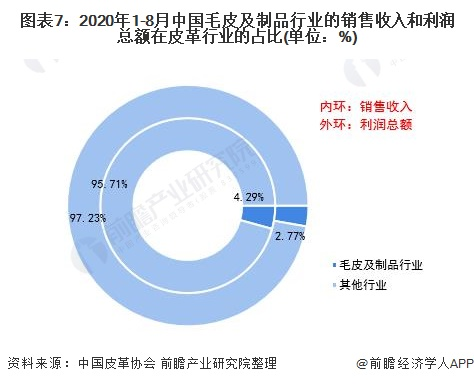

In terms of the development of the fur and fur products industry, from January to August 2020, China's fur and fur products industry achieved sales revenue of 25.628 billion yuan, a year-on-year decrease of 29.89%, accounting for 4.29% of the leather industry; the total profit reached 897 million yuan, a year-on-year drop of 54.43%, accounting for 2.77% of the leather industry, showing an overall gloomy business performance.

Chart 7: Share of Sales Revenue and Total Profit of China's Fur & Fur Products Industry in the Leather Industry, Jan-Aug 2020 (Unit: %)

(3) Expanding Decline in the Output of China's Fur Garments

In terms of output, the output of fur garments in China fluctuated from 2016 to 2019, reaching 4.777 million pieces in 2019, a year-on-year increase of 24.63%. In 2020, affected by the COVID-19 pandemic, the industry's operating rate was low in the first quarter. The output of fur garments from January to August stood at 1.9884 million pieces, a year-on-year decrease of 28.25%, with the decline expanding by 1.76 percentage points compared with that from January to July.

Chart 8: Output and Growth Rate of China's Fur Garments, 2016-2020 (Unit: 10,000 pieces, %)

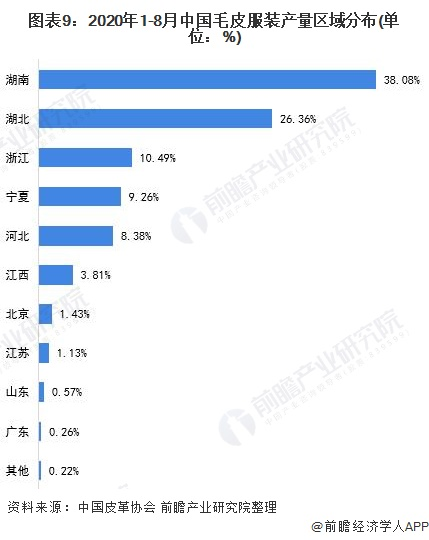

(4) Hunan Province Boasts the Largest Market Share in Fur Garment Output

In terms of the regional distribution of fur garment output, Hunan Province is the largest production base of fur garments in China, with its output accounting for 38.08% of the national total from January to August 2020; followed by Hubei Province with a share of 26.36%; Zhejiang Province ranked third with 10.49%. The output share of all other provinces was below 10%.

Chart 9: Regional Distribution of China's Fur Garment Output, Jan-Aug 2020 (Unit: %)

5. China as a Major Power in Fur Trade

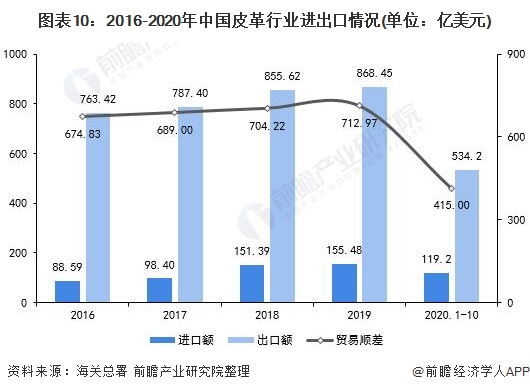

With the development of the fur industry, China has played an important role in the global fur trade. At present, China is the world's largest processor and exporter of fur garments. The rapid development of China's economy has strongly driven the growth of fur product consumption. In 2019, China's import and export volume of leather reached 15.548 billion US dollars and 86.845 billion US dollars respectively, achieving a trade surplus of 71.297 billion US dollars.

In recent years, China's leather export market has performed well, with the trade surplus growing continuously. From January to October 2020, China's import and export volume of the leather industry reached 11.92 billion US dollars and 53.42 billion US dollars respectively, a year-on-year decrease of 7.6% and 24.1% respectively, mainly due to the impact of the COVID-19 pandemic. With the overseas pandemic still not under effective control, the export situation of China's leather industry remains grim.

Chart 10: Import and Export of China's Leather Industry, 2016-2020 (Unit: 100 million US dollars)

In terms of the fur export market, from January to October 2020, China's export volume of fur garments was 2.8268 million pieces with an export value of 1.646 billion US dollars, both showing a year-on-year decrease. The export volume of raw hides reached 14,680 tons with an export value of 14 million US dollars, both registering a year-on-year increase.

In terms of the import market, from January to October 2020, China's import volume of fur garments was 19,100 pieces with an import value of 28 million US dollars, both falling year-on-year; the import volume of raw hides reached 1.1001 million tons, a year-on-year increase of 15.5%, with an import value of 826 million US dollars, a year-on-year drop of 15.1%, indicating a sharp decline in the average import price.

Chart 11: Import and Export of China's Fur Industry, 2019 and Jan-Oct 2020 (Unit: 10,000 pieces, 10,000 tons, 100 million US dollars, %)

6. Building Strong Brands to Enhance China's International Influence in the Fur Industry

At present, the offline sales of fur in China are mainly conducted through factory-owned direct stores or regional agents, and enterprises also participate in trade fairs in various domestic cities to attract new customers, such as the China Import and Export Fair, the China International Fur and Leather Products Fair and so on. The main online channels include industry self-media platform Pilele, the China Leather and Fur Trading Platform APP, the China Leather Network and other platforms.

Driven by policies and the market, a number of outstanding enterprises have emerged in China's fur industry, such as Shandong Hengtai, Zhejiang Zhonghui, Zhejiang Snow Leopard and so on. With personalized consumption, fashion consumption, quality consumption and brand consumption gradually becoming the pursuit of the new generation of consumers, China's fur enterprises have been continuously upgrading their brands and innovating their products to build international brand influence.

Chart 12: Major Enterprises in China's Fur Industry

Note: The ranking is in no particular order.